Why Today’s Inflation Is a Supply-Side Story

January 10, 2023

By Ira Regmi

Since March 2022, the US Federal Reserve has pursued aggressive interest rate hikes in an attempt to curb inflation. However, not only do these increases fail to address the true causes of today’s inflation, they will also raise unemployment and inflict significant, disproportionate harm on marginalized communities. The argument that higher unemployment is the necessary but unfortunate consequence of reducing inflation lacks consideration of the real consequences of this type of aggressive monetary policy, as well as the context of this particular recovery.

In a recent paper, The Causes of and Responses to Today’s Inflation, Joseph Stiglitz and I explain that the inflation we’ve been seeing comes from various supply-side issues and sectoral demand shifts rather than massive increases in aggregate demand. This means that there is a fundamental problem-solution mismatch: The primary channel through which the Fed hopes to bring down inflation is aggregate demand, but this strategy ignores the true causes of current inflation.

Specifically, the labor market is the primary mode of operation for interest rate hikes, meaning the Fed depends on increasing unemployment to address inflation. But this mechanism has limited room for precision in targeting specific pain points or sectors. This makes it a rather blunt tool that relies on a systemic agreement that the most marginalized communities are the most harmed, illustrating the structural racism embedded in our economic and political systems.

For example, because the unemployment rate for Black Americans, on average, runs two times higher than for white Americans, the projected rate of unemployment as a result of interest rate hikes would therefore be two times higher for Black Americans. This is similar to what we saw during the Great Recession, when the unemployment rate for Black Americans peaked at 15 percent in April 2009, while white unemployment was around 8 percent.

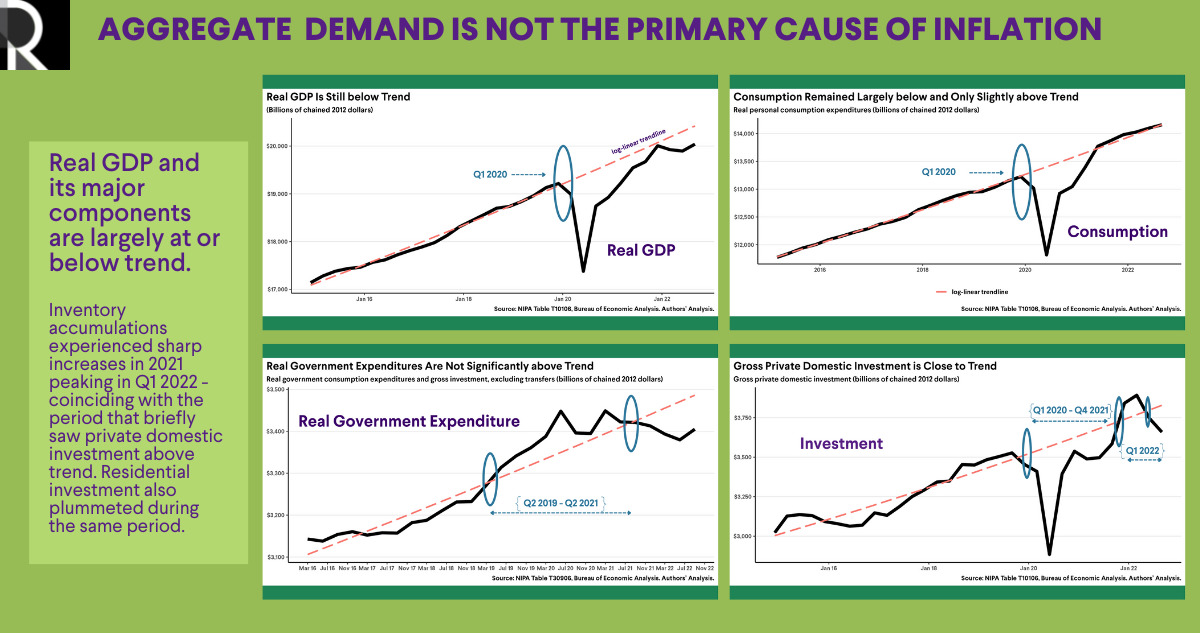

Aggregate Demand Is Not the Primary Cause of Inflation

Our paper highlights how the orthodox understanding of a stable relationship between inflation and unemployment is obsolete and does not apply to the current situation; using unemployment to control inflation is therefore misguided.

We also rebut the idea that price increases are due to increased demand as a result of pandemic stimulus. The first problem with this argument is empirical—data on savings show that people did save stimulus money, and personal savings rates remained above pre-pandemic levels until late 2021, well after inflation started to increase. While these “excess” savings did dip after April 2022 once the economy gradually reopened, there isn’t a one-to-one relationship between the depletion of savings and aggregate demand, showing that not all of this reduction in excess savings went toward demand and consumption of goods and services. In fact, a part of the reduction in savings actually came from the payment of non-withheld taxes applicable to capital gains (including forms of dividends), which surged in 2021.

Moreover, people in the bottom 25 percent of the income distribution experienced the most significant increase in median weekly cash balances—52.9 percent between January 2020 and June 2022—which suggests that the households that experienced a strong material difference in disposable income due to the pandemic stimulus spent the least of that money. Had the American Rescue Plan been a primary source of inflation, we would have seen an increase in consumption from the households that benefited most from it.

In addition, components of output, including consumption, investment, government expenditure, and net exports, all remain mostly at or below pre-pandemic trends, especially when accounting for the peculiarities in inventory buildup and residential investment. This suggests little evidence of excess aggregate demand. For instance, the brief period in which investments were slightly above trend in 2022 saw a dramatic increase in inventory accumulation—also a feature of supply chain disturbances. In addition, part of the excess savings directed toward consumption had a relatively restrained impact on overall output, as globally traded goods and record corporate profits meant a smaller multiplier effect. Consumption of domestically produced goods fuels stronger income growth, which then further fuels and in a way multiplies demand and consumption more than what the initial result would have been.

Supply-Side and Sector-Specific Inflationary Pressures

Our paper also highlights the various supply-side issues that dominated inflationary pressures in 2022, especially those in the energy and food sectors. Due to the inherent volatility of fossil fuel prices and the Russian invasion of Ukraine in February 2022, energy prices soared to almost two times pre-pandemic levels in June 2022. Market concentration and manipulation in the food market caused prices to increase throughout 2020 and were further fueled by geopolitical disturbances in 2022. Price increases in the energy and food sectors or shortages in certain industries (such as shortages of semiconductor chips) can cause shifts in the demand patterns in other industries (such as automobiles). Supply shocks like COVID-19 can also directly alter patterns of demand. This happened with the housing market, which saw changes in the type, size, and geographic location of demand.

Disruptions from the COVID-19 pandemic also exposed and aggravated weaknesses in the supply chain demonstrated by the rapid rise in the share of the prices of core goods since 2021 and its subsequent decline as inflation began to stabilize. Our analysis of the CPI data shows that core goods, which exclude energy and food and are especially sensitive to supply chain disturbances, contributed 2.3 percentage points (p.p.) to inflation in 2021. By October 2022, as supply side pressures began to ease, core goods’ contribution to inflation dropped to 1.8 p.p.. By November, without declining demand, we have seen two consecutive months of core goods deflation with no increases in automobile prices in November—a category that drove 1.9 p.p. of the core goods’s share of inflation in 2021.

Increased market concentration and market power played a role in reducing the resiliency of supply chains. Our paper demonstrates how a lack of competition enabled firms to prioritize short-term profit gains over longer-term investment in supply chain efficiency. Large increases in share buybacks also resulted in profits being directed away from investments, making supply chains less resilient.

Weakened supply chains are only one of the impacts of increased market power. Rising aggregate markups and soaring corporate profits all signal that increasing consumer prices reflect more than just increases in costs of production—private corporations, especially in recent years, have passed on more than just the increases in costs of production to consumers. Even as inflationary pressures have decreased, firms have openly boasted of increased profits under cover of inflation.

Third, they identify 5 intermixed factors causing inflation:

➡️energy and food

➡️ supply interruptions

➡️demand shifts in the presence of supply inelasticities

➡️increased rents from a shift in housing demand

➡️manifestations of market power.All these are the key. (4/8) pic.twitter.com/9uUIdTNUpr

— Roosevelt Institute (@rooseveltinst) December 6, 2022

Labor Market Tightness and Wages

Conventional macroeconomics points toward a stable relationship between unemployment and wage inflation, but there are various reasons why this may not necessarily be true. Wage increases may result from demographic changes, search and turnover costs, or the kind of supply shocks we saw during the COVID-19 pandemic. With large enough sectoral disturbances, reliance on macroeconomic relationships established in the past, say between unemployment and inflation, can lead to a problem-solution mismatch in the present.

In our paper, we argue that moderating nominal wages and, more importantly, declining real wages are not signifiers of a wage-price spiral. If labor shortages exist, policy responses should focus on increasing labor supply, not decreasing aggregate demand. It is essential to understand that declining real wages should be a cause for concern, not celebration. If macroeconomic theory does not give us room to celebrate wage increases—especially for those who earn the least—the solutions it proposes must be reconsidered.

Looking Ahead

By accepting raising interest rates as the ultimate solution to inflation despite this tool’s bluntness, ineffectiveness, and the large risks it poses to communities, modern economics finds itself on a tightrope, balancing a line between discipline and theology. It is a mistake to assume that the evolution of the modern financial sector and the shock of a massive global pandemic have not altered the transmission channels through which modern economics assumes rate hikes work. The ability to wield interest rates with any precision to target specific pain points should have always been in question, as should the unreliability induced by the large lags with which monetary policy operates.

While our paper presents a case for the inflationary pressures from sectoral supply-side issues and the resulting changes in patterns of demand, we also point out that it is impossible to completely parse the exact distribution of supply-side and demand-side contributions to inflation. Aggressive rate hikes have already and will continue to result in much pain for many people with little to no benefit. On the other hand, fiscal policy and other targeted measures that increase investment, curtail market power, and ensure the provision of essential services will alleviate supply chain issues to address inflation and provide long-term benefits to people.

Author